First Sale Valuation: The Complete 2026 Guide for Importers

TL;DR

1. What First Sale Actually Does

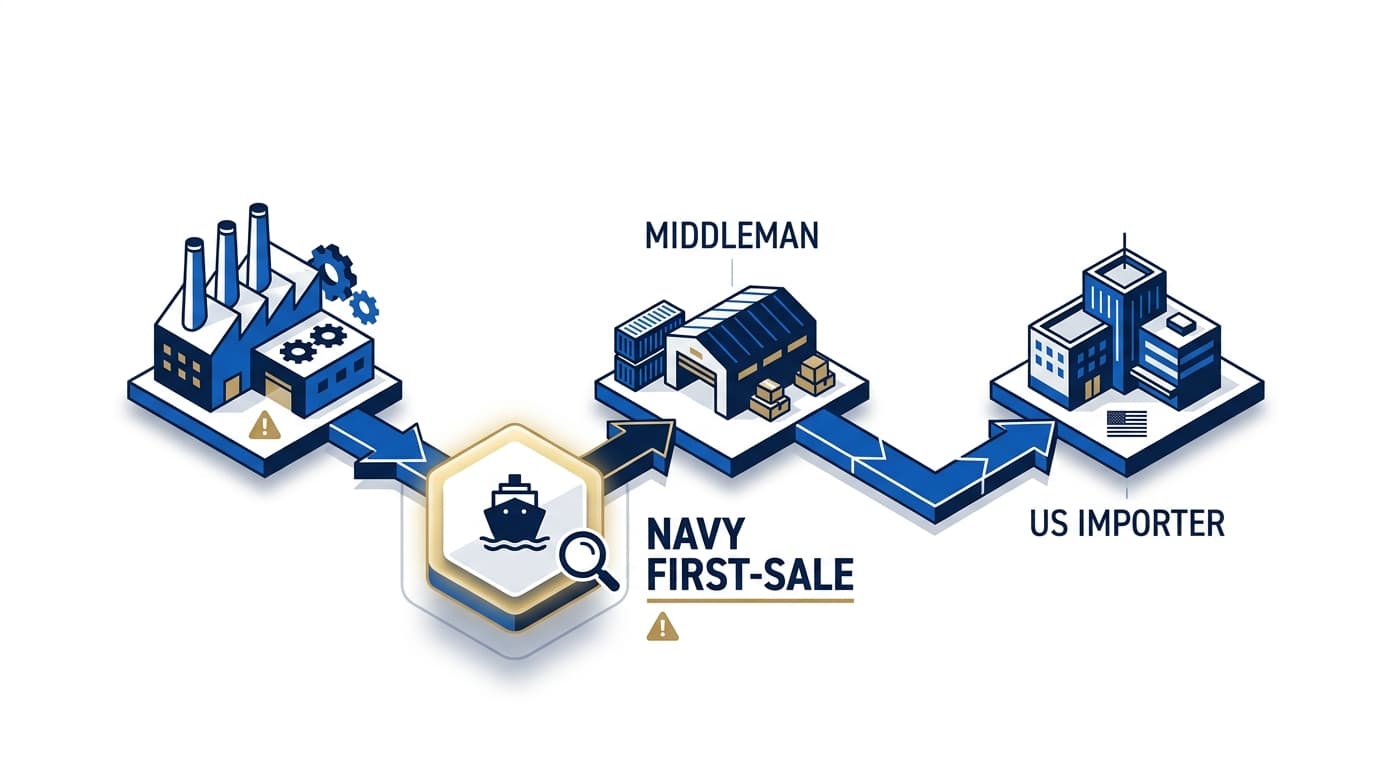

In a typical multi-tier import, the supply chain looks like:

Factory (China) → Trading Company (Hong Kong) → U.S. Importer

The factory sells to the trading company at $100 per unit. The trading company marks up and sells to the U.S. importer at $140 per unit. Under the default U.S. valuation rule (transaction value to the buyer), the U.S. importer declares $140 as the customs value and pays duty on $140.

Under First Sale, the U.S. importer declares $100 (the first sale) as the customs value and pays duty on $100. The $40 middleman markup is excluded from the dutiable base, reducing duty by 28.6%.

Across a typical 7.5% Section 301 list + 10% IEEPA stack + 4% MFN, First Sale can reduce total duty outlay by 20-40% on imports structured through trading companies.

2. The Legal Framework

The core authority is Nissho Iwai American Corp. v. United States, 982 F.2d 505 (Fed. Cir. 1992), which held that in a multi-tier transaction, the U.S. importer may declare the first sale price if the importer can prove:

- A bona fide sale between the factory and the middleman.

- Goods clearly destined for the United States at the time of the first sale.

- An arm's-length transaction between factory and middleman.

- Accurate documentation supporting all of the above.

CBP codified the framework in the ruling HQ 546932 (1997) and subsequent guidance, now part of 19 CFR 152.103 and CBP's Informed Compliance Publication "What Every Member of the Trade Community Should Know About: Customs Value."

Additional technical requirements:

- The first sale price must reflect the actual transaction between factory and middleman (not a constructed price).

- The middleman must take title (even briefly) or bear risk of loss.

- Any commissions, licensing fees, or assists flowing from the importer to the factory must be added back under 19 USC 1401a(b)(1).

- Documentation must be contemporaneous and auditable for five years.

3. When First Sale Is Worth Pursuing

First Sale pays off when three conditions align:

1. Multi-tier structure. If the U.S. importer buys directly from the factory, there is no first sale to declare. The factory price is the only price. First Sale requires a genuine middleman.

2. Meaningful markup. The economics only work if the middleman's markup is large enough to cover First Sale implementation costs. Rule of thumb: markup ≥ 15% and annual import volume ≥ $2M.

3. High duty rate. Savings scale with the total duty rate. On MFN-only imports at 3-5%, First Sale may save $60K per $1M of markup excluded. On Section 301 + IEEPA stacks at 25-40%, the same $1M markup exclusion saves $250-400K.

4. Documentation Required

CBP audits First Sale aggressively. A complete documentation package for each first-sale entry must include:

| Document | Purpose | Source |

|---|---|---|

| Factory invoice to middleman | Establishes first sale price | Factory |

| Factory commercial invoice | Corroborates first sale amount | Factory |

| Middleman purchase order to factory | Shows transaction terms | Middleman |

| Evidence of payment factory ← middleman | Proves actual sale | Bank records |

| Middleman invoice to U.S. importer | Shows second sale | Middleman |

| Bill of lading with U.S. as destination | Proves goods destined for U.S. | Carrier |

| Inspection certificate | Corroborates U.S. destination | QC firm |

| Middleman P&L showing markup retention | Proves arm's-length | Middleman |

| POA and assist statements | Addresses related-party and assist risks | Importer |

In related-party transactions (where factory and middleman share ownership), CBP applies heightened scrutiny and may reject First Sale absent a rigorous arm's-length analysis using one of the tests in 19 USC 1401a(b)(2)(B).

5. How to Implement First Sale

Implementation is an 8-step program:

Step 1: Map your supply chain. Identify every tier between factory and U.S. entry. First Sale applies only where a genuine middleman exists.

Step 2: Feasibility analysis. Run duty simulation with and without First Sale. Use the First Sale Savings Calculator. Require 15% minimum markup and $2M+ annual volume to justify setup cost.

Step 3: Counterparty alignment. Your middleman must agree to share factory invoices with you. Some trading companies refuse; their margin is visible to you and potentially to CBP. Negotiate this upfront or walk.

Step 4: Ruling request. For complex multi-tier structures, request a binding ruling from CBP (HQ Valuation Branch) under 19 CFR Part 177. Rulings take 90-180 days but provide certainty.

Step 5: Entry summary code. File entries with value on CBP Form 7501 declared at the first sale price. Indicate First Sale in the entry summary instructions to your broker.

Step 6: Documentation hub. Build a recordkeeping system that pulls factory invoices, middleman PO, and BOLs per entry. CBP will CF-28 test the package within 6-12 months of implementation.

Step 7: Annual audit. Run an internal First Sale compliance audit annually. Look for: missing factory invoices, markup anomalies, related-party risk signals.

Step 8: Maintain for 5 years. Records must be retained five years from date of entry per 19 CFR 163.4.

6. The Cassidy Bill Threat

Senator Cassidy (R-LA) introduced S. 2987 in March 2026, which would:

- Eliminate First Sale valuation for goods from non-market economies (China, Vietnam, specified others).

- Require U.S. importers to declare the "last sale" price (the price to the U.S. importer) regardless of upstream structure.

- Apply prospectively from date of enactment, with a 180-day implementation window.

The bill has bipartisan co-sponsors and has advanced out of the Senate Finance Committee. If enacted, First Sale would become unavailable for the largest source country (China), which would significantly reduce its value for most importers.

Implication: importers considering First Sale should implement now and capture savings during the window before potential legislative change, while maintaining documentation robust enough to survive any retroactive enforcement challenge. Binding rulings obtained before the bill's enactment date generally carry grandfather protection under 19 CFR 177.9.

7. How First Sale Interacts with IEEPA Refunds

For entries filed between April 2, 2025 and February 20, 2026, importers who used First Sale declared customs value at the first sale price, and IEEPA duty was calculated against that lower base. The IEEPA refund via CAPE recovers 100% of that duty, identical in mechanics to non-First-Sale entries.

If you did not use First Sale during that period and paid duty on the higher marked-up value, you cannot retroactively amend the valuation to First Sale during the CAPE refund process. However, you can file Post-Summary Correction on any unliquidated entries within 300 days of entry, potentially combining First Sale amendment with IEEPA refund. Check eligibility on the AI Analyzer.

8. Common First Sale Mistakes

- Constructed first-sale price. Claiming a first sale that did not actually occur (factory and middleman under common control, no real transaction). CBP treats this as fraud under 19 USC 1592.

- Missing destination evidence. If BOLs show transshipment through a non-U.S. port without U.S. destination markers at the factory, CBP rejects First Sale.

- Assists not added back. Tooling, molds, design costs provided by the U.S. importer must be added to the first sale price under 19 USC 1401a(b)(1)(C). Omitting these is a recurring violation.

- Related-party transactions without arm's-length proof. CBP presumes non-arm's-length in related-party deals unless proven otherwise.

- Stale rulings. Rulings issued more than 5 years ago and not updated may be revoked as facts change.

Frequently Asked Questions

Q: Does First Sale work for direct factory imports? No. First Sale requires a multi-tier transaction with a genuine middleman. Direct factory imports use transaction value at the factory price, which is already the lowest value.

Q: How much can First Sale save? On a typical 25% markup and 25% combined duty rate, First Sale saves about 6.25% of import value. Annual savings scale with volume; a $20M/year importer commonly saves $1.2-1.5M.

Q: Does First Sale survive the Cassidy bill? For non-China imports, likely yes. For China imports, the bill would eliminate First Sale. Timing matters.

Q: Do I need a binding ruling? Not strictly, but highly recommended for multi-tier structures, related parties, or any valuation above $5M/year. A ruling prevents retroactive assessment.

Q: Can my broker file First Sale on my behalf? Yes. First Sale declaration is part of entry filing; your licensed customs broker handles it under 19 USC 1641. You must provide the documentation.

Estimate your savings: Try the First Sale Savings Calculator, upload your invoices to the AI Analyzer, or book a feasibility consult.

Reviewed by Licensed Customs Broker Partner (pending name). Last updated April 22, 2026. Educational content only. First Sale classification and entry filing are customs business executed by our partner licensed customs broker under 19 USC 1641.

Keep reading

first-sale legality and CBP rulings

Quick answer on whether first-sale survives scrutiny.

Read more →

tariff-engineering as a future-entry strategy

Companion strategy that pairs with first-sale planning.

Read more →

HTS reclassification deep dive

Classification strategy alongside valuation strategy.

Read more →

apparel industry first-sale opportunities

Vertical with the highest first-sale density.

Read more →Frequently asked questions

Ready to recover?

Run the calculator or take the 60-second qualification quiz. Estimate only — subject to CBP adjudication.