How to File a Duty Drawback Claim: Step-by-Step 2026 Guide

TL;DR

1. What Drawback Actually Is

Drawback is the oldest refund mechanism in U.S. customs law, first enacted in the Tariff Act of 1789. It exists because the U.S. does not want to tax exports: if you pay duty on an imported component and then export the finished good, you should get that duty back. Modern drawback, governed by 19 U.S.C. § 1313 and 19 CFR Part 190 (post-TFTEA rewrite), refunds 99% of duty paid, with 1% retained by CBP as administrative fee.

Drawback covers:

- Regular ad valorem duties (MFN)

- Section 301 China duties (confirmed refundable through substitution per CSMS 42421561)

- Section 232 steel/aluminum duties (limited to direct identification manufacturing drawback; substitution barred by §232 proclamation)

- Section 201 safeguard duties

- IEEPA duties (where the import predates the SCOTUS ruling and export occurred before the CAPE remedial window; double-refund is barred)

- Merchandise Processing Fee (MPF) and Harbor Maintenance Fee (HMF)

Drawback does not cover antidumping or countervailing duties under 19 U.S.C. § 1673.

2. The Three Drawback Types, Compared

| Type | Statute | What Triggers It | Key Constraint |

|---|---|---|---|

| Manufacturing (Direct ID) | §1313(a) | Imported merch used to make an exported article | Must trace lot-by-lot |

| Manufacturing (Substitution) | §1313(b) | Substituted merch of same 8-digit HTS used to make exported article | 8-digit HTS match required |

| Unused Merchandise (Direct ID) | §1313(j)(1) | Imported merch exported without being used domestically | Must trace identical unit |

| Unused Merchandise (Substitution) | §1313(j)(2) | Substituted merch of same 8-digit HTS exported unused | 8-digit match, 3-year window |

Substitution drawback is the workhorse for most importers because it does not require lot-level traceability of the specific imported unit. Any unit of merchandise with the same 8-digit HTSUS classification can be substituted.

See Substitution vs Manufacturing Drawback for a decision tree.

3. Filing Prerequisites

Before you file your first claim, you need:

1. ACE Drawback Account. File CBP Form 5106 (Importer ID Input Record) if you are not already an IOR. Drawback claimants must have a CBP-assigned IRS or SSN ID.

2. Continuous Bond with Drawback Rider. Standard continuous bond under 19 CFR 113 does not automatically cover drawback. You need a Type 1A drawback bond or a rider on your Type 1 import bond.

3. Accelerated Payment Privilege (APP). Without APP, refunds take 12-24 months. With APP, refunds arrive in 4-6 weeks. Apply via CBP Form 301 or the ACE Drawback module. APP requires a bond at 100% of the annual drawback projection.

4. Manufacturing Ruling (for §1313(a) and (b)). General manufacturing rulings cover common processes (roasting, blending, assembly). Specific rulings are filed on CBP Form 7553 with a detailed bill of materials and process description. Rulings take 6-12 months; start early.

5. Privileges Application. Waiver of prior notice (for unused merchandise drawback) and one-time waiver for destruction claims must be applied for separately via ACE.

4. The Documentation Matrix

Every drawback claim must be supported by a documentation package CBP can audit for five years after the claim liquidates. The matrix below shows what each claim type requires:

| Document | §1313(a) | §1313(b) | §1313(j)(1) | §1313(j)(2) |

|---|---|---|---|---|

| CBP Form 7501 (import entry) | Yes | Yes | Yes | Yes |

| Commercial invoice, import | Yes | Yes | Yes | Yes |

| Bill of materials | Yes | Yes | No | No |

| Manufacturing records | Yes | Yes | No | No |

| Inventory receipt and draw records | Yes | Yes | Yes | Yes |

| Export documentation (BoL, AES filing) | Yes | Yes | Yes | Yes |

| Manufacturing ruling on file | Yes | Yes | No | No |

| Certificate of Delivery (CD) | If using | If using | If using | If using |

| Certificate of Manufacture and Delivery (CMD) | Yes | Yes | N/A | N/A |

| Notice of Intent to Export/Destroy | N/A | N/A | If required | If required |

All records must be retained for three years after payment of the drawback claim under 19 CFR 190.15, though audit experience suggests keeping them five to seven.

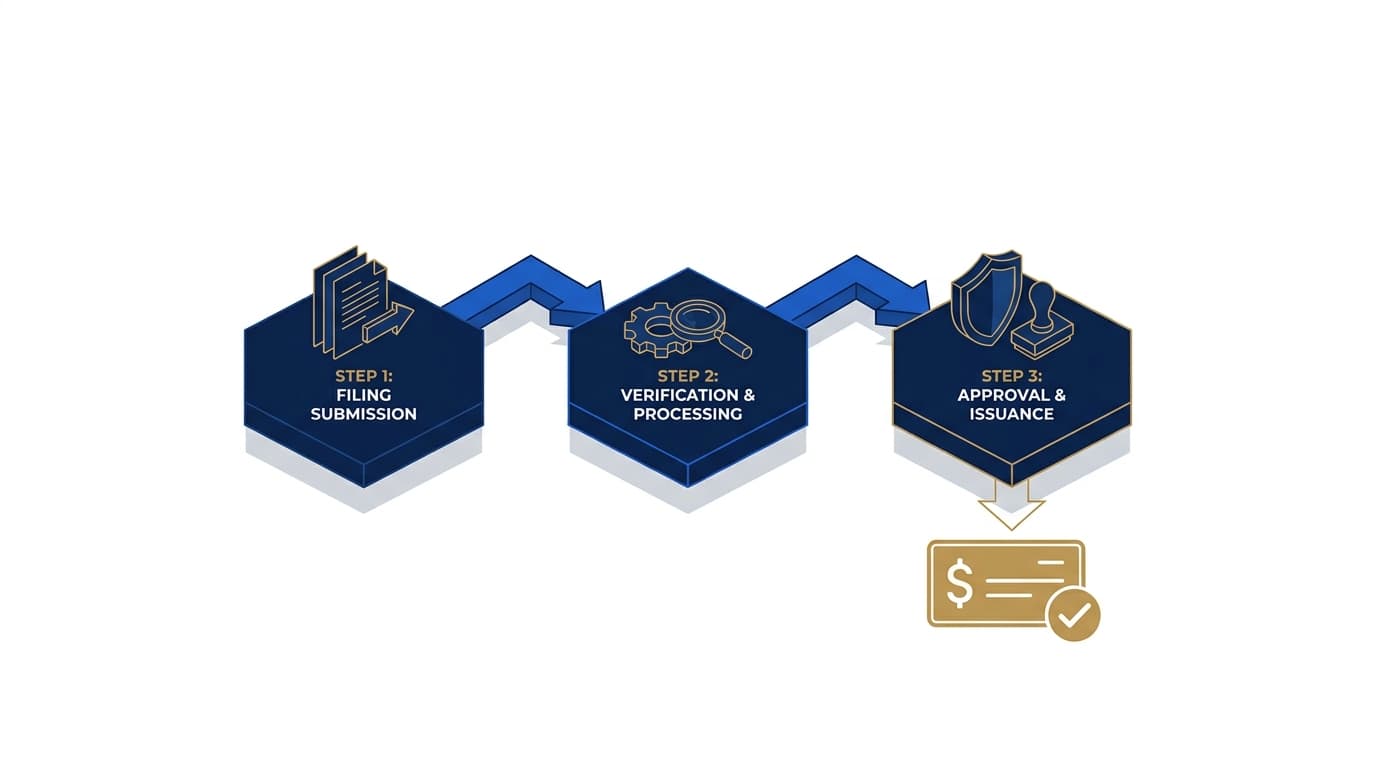

5. Step-by-Step Filing Process

Step 1: Pull import entries. Export ACE entry summary data for the period you are claiming. Filter for entries with duty, MPF, HMF, and relevant Section 301/232 charges. Identify the 8-digit HTSUS and duty paid per line.

Step 2: Pull export records. From your AES (Automated Export System) filings, pull EEI (Electronic Export Information) records for the same period. Match 8-digit HTSUS exported to 8-digit HTSUS imported for substitution claims.

Step 3: Calculate the refund. For each matched import/export pair, compute 99% of (duty + MPF + HMF) attributable to the exported quantity. The Drawback Estimator will do this automatically if you upload your ACE and AES CSVs.

Step 4: Build the claim file. The ACE drawback module accepts CSV upload or interactive entry. For bulk claims, CSV is standard. Each claim line references the import entry, export entry, HTSUS, quantity, and claimed amount.

Step 5: Privileges and bond check. Confirm APP is approved and drawback bond is sufficient before submission.

Step 6: Submit via ACE. The drawback claim is assigned a claim number. Acknowledgement returns in minutes; liquidation occurs in 12-18 months absent APP.

Step 7: If APP approved, accelerated refund arrives in 4-6 weeks. CBP may still perform a post-payment audit. Maintain your documentation.

Step 8: Respond to any CF-28 (Request for Information) or CF-29 (Notice of Action) within the deadline, usually 30 days.

6. Common Mistakes

- Missing the 5-year deadline. Under 19 U.S.C. § 1313(r), claims must be filed within five years of date of import. TFTEA clarified this to mean five years from import, not from export.

- 8-digit HTSUS mismatch. Substitution requires identical 8-digit classification. 10-digit differences are fine; 8-digit differences disqualify.

- Filing before APP is approved. Claims without APP sit in the queue for up to 24 months.

- No manufacturing ruling. §1313(a) and (b) claims filed without a ruling are rejected.

- Claiming on AD/CVD duties. These are not drawback-eligible.

- Export without AES filing. No AES = no export proof = no drawback.

- Double-claiming IEEPA duty through both CAPE and drawback. Pick one path per dollar of duty.

7. How the 2026 CAPE Interaction Works

With the IEEPA ruling and CAPE portal in play, drawback claimants must not double-refund the same IEEPA dollar. CBP's CSMS 62104411 explicitly bars duplicate recovery: if you received an IEEPA refund via CAPE or CF-19, you cannot also claim drawback on that duty. Section 301 and Section 232 duties are not affected and remain drawback-eligible.

Practical rule: if the import entry paid both IEEPA and Section 301 duty and the merchandise was exported, file CAPE for the IEEPA portion and drawback for the Section 301 portion. Two separate refunds, one per statutory basis. Use the AI Analyzer to auto-split your entries.

8. Timeline and Cash Flow

With APP:

- Day 0: file claim in ACE

- Day 5-10: CBP acknowledges receipt

- Day 30-45: accelerated refund disburses via ACH

- Month 12-18: CBP liquidates the claim (final audit window)

- Month 18-24: any post-liquidation recovery if audit reduces

Without APP:

- Day 0: file

- Month 12-18: liquidation and refund in same cycle

- Interest accrues on liquidated claims not paid within 30 days of liquidation per 19 U.S.C. § 1505(c)

Frequently Asked Questions

Q: What is the drawback deadline? Five years from date of import under 19 U.S.C. § 1313(r). Export must occur before the claim is filed and generally within the same 5-year window.

Q: Can I claim drawback on Section 301 China duties? Yes, both direct identification and substitution drawback are allowed on Section 301 duties per CSMS 42421561.

Q: Do I need a licensed customs broker to file drawback? If you file for your own company as the IOR, no. If a third party files for you for compensation, that third party must be a licensed customs broker under 19 USC 1641.

Q: How long does accelerated payment actually take? With APP approved and a clean claim, 4-6 weeks from submission to ACH deposit.

Q: Can I amend a drawback claim after filing? Yes, via an amended claim filing before liquidation. After liquidation, the 180-day protest window under 19 USC 1514 applies.

Next step: Run your numbers on the Drawback Estimator or book a call with our licensed customs broker partner to scope the engagement.

Reviewed by Licensed Customs Broker Partner (pending name). Last updated April 22, 2026. Educational content only. Drawback filings should be executed by a licensed customs broker under 19 USC 1641.

Keep reading

what drawback brokers charge

Cost framework before you engage a filer.

Read more →

drawback versus the standard refund route

Quick framing of the two parallel paths.

Read more →

FTZ strategy alongside drawback claims

When zone designation pairs with drawback recovery.

Read more →

merchandise processing fee refund mechanics

Pro-rata fee inclusion in drawback claims.

Read more →

Ohio drawback filing context

Drawback mechanics for export-oriented OH plants.

Read more →Frequently asked questions

Ready to recover?

Run the calculator or take the 60-second qualification quiz. Estimate only — subject to CBP adjudication.